FRBの財布の中身

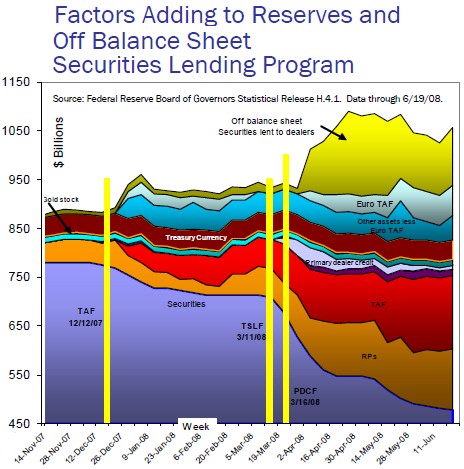

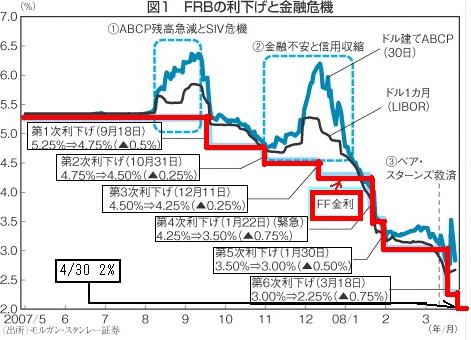

すでに真水(Cash)が半減したFRBの財布SOMA、 パッと見で、総額が増えてんだけど、これ如何に? Bigpictureより、 Reserves and Off Balance Sheet Securities Lending Factors Adding to Reserves and Off Balance Sheet Securities Lending Program (pdf)Explanation of Factors Adding to Reserves ChartThe Federal Reserve Board has posted on its website information on how its balance sheet was allocated across the different asset classes, as well as the composition of its liabilities. For many years prior to the most recent turmoil that has occurred in financial markets, the bulk of the Federal Reserve’s assets were in the form of its holdings of US Treasury securities. Nearly 90% on average of its assets were of this type. Other major asset categories included Treasury currency and the gold stock. Normal daily open-market operations which add to and subtract from the Federal Reserve’s balance sheet take place mainly through repurchase and reverse repurchase agreements.The composition of the Federal Reserve’s portfolio has, however, changed dramatically during the recent period of financial turmoil, as the Board of Governors has modified the terms under which access to the discount window is available to banks, and now to investment banks, and the FOMC has modified its securities lending program from the System Open Market Account (SOMA).Specifically, four new programs have been created:Term Discount Window Program (TDWP) – announced August 17, 2007Under the TDWP banks were permitted to borrow on the full range of eligible discount window collateral for a term of up to 90 days.Term Auction Facility (TAF) – announced December 12, 2007Under the TAF banks were permitted to bid for term federal funds with maturities up to 28 days, backed by the full range of eligible discount window collateral.Term Securities Lending Facility (TSLF) – announced March 11, 2008Under the TSLF primary dealers (both banks and investment banks) were permitted to borrow US Treasuries from the SOMA portfolio overnight for a term of up to 28 days, using Treasuries, agency securities, agency mortgage-backed securities, AAA/Aaa-rated private-label real estate MBS, collateralized MVS, agency-collateralized mortgage obligations, and other asset-backed securities (these latter securities were added to the list on May 2, 2008). The Treasury securities so borrowed could then be repo-ed overnight and used as a way of liquefying what might otherwise be illiquid assets in this period of market turmoil. The TSLF-related securities lent show up on the System’s balance sheet as offbalance-sheet items.While the Federal Reserve has attempted to sterilize the impact of its lending programs so as to avoid undue expansion of the money supply, we do not believe that this adequately represents the total expansionary impact of the Federal Reserve's efforts to deal with the problems in certain segments of financial markets. The System has also initiated, in addition to its regular securities lending program, the Term Securities Lending Facility.This Facility permits prime dealers to borrow securities from the Federal Reserve's portfolio for a term of up to 28 days. In a series of rolling overnight loans of securities, prime dealers are permitted to pledge a wide range of eligible collateral (Treasuries, agencies, agency MBS, AAA/Aaa-rated private-label RMBS, CMBS, agency CO and other ABS) in return for US Treasuries which they can then RP out overnight. The effect is to enable them to liquefy otherwise illiquid securities on their balance sheets and replace them with dollar assets which can then be deployed in other ways. While these assets represent a reallocation of reserves within the US banking system, they also represent a way for prime dealers to tap into dollar reserve assets from the rest of the world. To the extent that prime dealer assets are freed up, these institutions can engage in lending that would otherwise not occur. Securities lent under the TSLF are off the Federal Reserve's balance sheet since the transaction is unwound each morning. During the day, the funds that had been RPed by the prime dealers is likely replaced by daylight overdrafts from the Federal Reserve. Thus, there is effectively an off balance sheet creation of additional reserves to the banking system. To reflect the potential expansionary impact of the TSLF, we have created Chart 2, which attempts to reflect the potential impact that the TSLF may be having on the banking and financial system by adding the TSLF memorandum item to the Federal Reserve's balance sheet. Primary Dealer Credit Facility (PDCF) – announced March 16, 2008Under the PDCF primary dealers (both banks and investment banks) were permitted to borrow at the discount window using US Treasuries, agency securities, agency mortgagebacked securities, and investment-grade debt facilities.The documentation for these programs and weekly balance sheet effects can be gleaned from the Federal Reserve’s H.4.1 data release and are the basis for the information contained in the chart shown on Cumberland’s website. We have followed the unusual procedure of adding the Memo Item Securities Lent to Dealers to the factors adding to reserves, despite the fact that these are off-balance-sheet items and technically don’t inject reserves into the banking system. However, because the securities lent to the primary dealers can be used to temporarily generate funds for these institutions that are pivotal in the monetary transmission mechanism and that have been at the core of the recent financial turmoil, the reallocation of funds within the banking system to these institutions is intended to be captured by recognition of these off-balance-sheet items. The Federal Reserve could have simply increased its balance sheet by the amount of the reserves lent, but this would not deal with the funding problems experienced by the primary dealers who were weighed down by holdings of high-grade but illiquid assets that brought the intermediation process to a standstill. So in this respect, the securities lending program was a targeted way to enable the primary dealers to resume activities that they might not have otherwise been able to do. 従来、90%は米国債が占めていたFRBの財布のSOMAだが、昨今ドラマティックに内容が変わった、90日迄延ばした証券担保貸出しTDWP、 28日証券担保貸出しTAF、 28日国債交換(証券会社OK)TSLF、 TSLFのUpdate版、各種担保OK、借入れ上限なしのPDCF、TSLF、PDCFで、リスクを取っている証券会社にまで連銀の窓口を作ってしまい、ここまできたかと言う感じだったが、それだけでなく実質、簿外扱いであったらしい(詳しいしくみはよくわからない、)これは、時が来れば業績が回復するので、それまでは一時的に財源をあることにして貸してしまおうと言うもの、ナルホド、これで財布が増えているわけか、(同じ要領でユーロTAFなんかもある、) で上のチャート見て思ったのは、簿外のTSLF、PDCFが損失になった場合、真水のUS国債がさらに減るのかしらって、 そして記事では、これは時間延ばしだけで本質的な解決策にはなっていないと、 (金の切れ目が縁の切れ目、) まさに綱渡り、 (参考)各Facilityについては、下記4/14付e株リポート(すでにリンク切れ)参照、但しTDWPを除く、 まず、FRBは昨年9月18日の利下げを皮切りに、4月30日までに7度にわたる利下げを断行、米政策金利のフェデラルファンド(FF)金利は、合計3・25%も引き下げられ、現在2・00%になっている。 FRBはさらに、期間28日の短期ドル貸出制度であるTAF(Term Auction Facility)および、ドルと他通貨を交換する為替スワップ(180日間)の導入を昨年12月12日に発表。同時に、欧州中央銀行(ECB)、スイス国民銀行(SNB)、イングランド銀行(BOE)およびカナダ銀行の欧米主要中央銀行と協調して流動性供給策に踏み切っている。 その後も3月11日には、プライマリー・ディーラー(証券会社)に対する米国債とMBS(不動産担保融資を裏付け債権として発行された証券)のスワップ制度である「TSLF(Term Security Lending Facility)」、同月16日には窓口貸し出し(公定歩合貸し出し)をプライマリー・ディーラーに開放する「PDCF(Primary Dealer Credit Facility)」を相次ぎ導入(表)。